Futures Market: Overnight, LME copper opened at $9,365.5/mt, initially bottoming out at $9,358.5/mt amid fluctuations. It then climbed to an intraday high of $9,429/mt before declining again, followed by a rebound forming a V-shape. Towards the close, the price center slightly moved downward, and it finally settled at $9,400/mt, up 0.42%. Trading volume reached 17,000 lots, and open interest stood at 296,000 lots. Overnight, the most-traded SHFE copper 2504 contract opened at 77,190 yuan/mt. The price center rose initially, peaking at 77,430 yuan/mt amid fluctuations, then fluctuated downward, bottoming out at 77,070 yuan/mt towards the close, before rebounding to settle at 77,310 yuan/mt, up 0.38%. Trading volume reached 24,000 lots, and open interest stood at 159,000 lots.

【SMM Copper Morning Brief】News: (1) According to CCTV, on Monday, March 3 local time, US President Trump announced that the 25% tariffs on goods from Mexico and Canada would take effect on March 4. Reciprocal tariffs would begin on April 2. Trump stated that there was no room for consensus on tariffs with Mexico and Canada. Additionally, Trump mentioned considering a free trade agreement with Argentina.

(2) Reliable sources revealed that China is studying and drafting countermeasures, which may include tariffs and a series of non-tariff measures, to respond to the US threat of imposing an additional 10% tariff on Chinese goods under the pretext of fentanyl. Among these, imposing tariffs on US-origin agricultural and food products is highly likely to be included in the countermeasures. The sources also indicated that if the US insists on unilaterally imposing additional tariffs and officially announces related measures, China will firmly implement strong countermeasures.

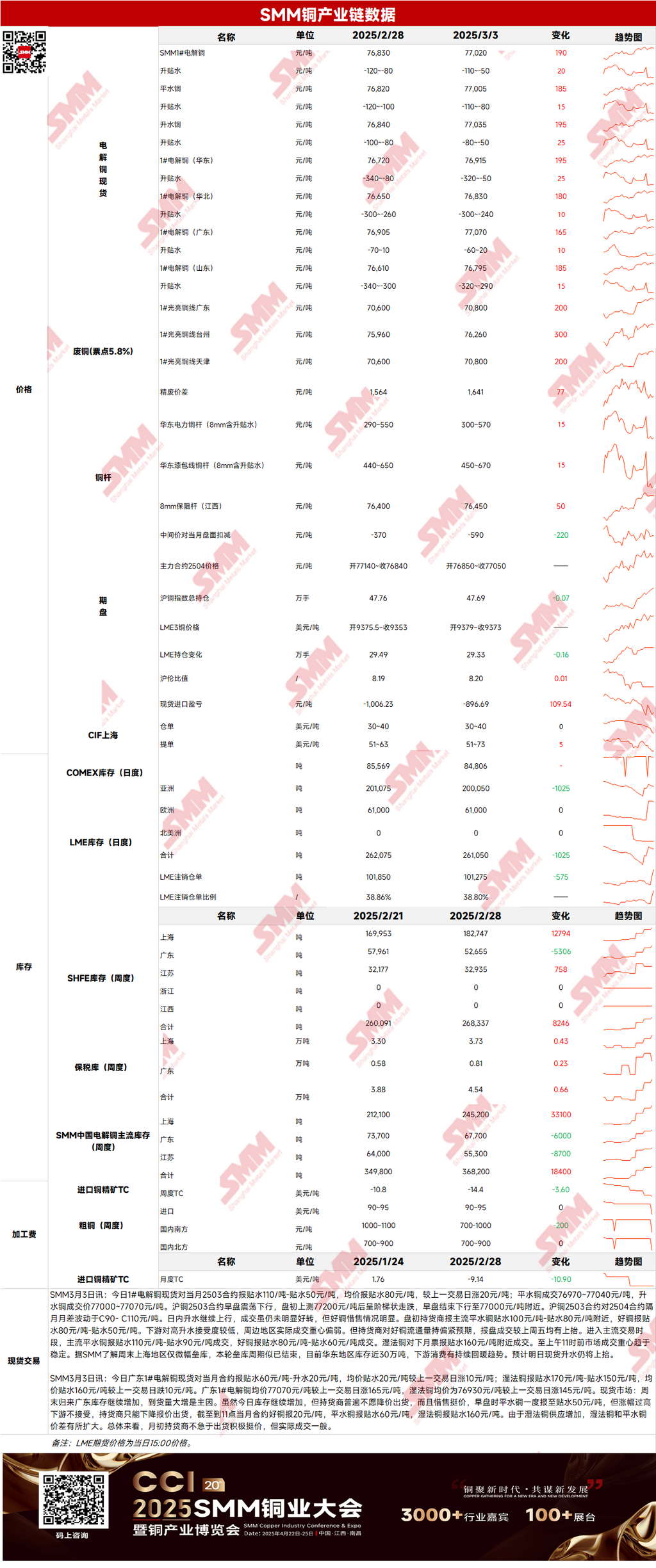

Spot Market: (1) Shanghai: On March 3, #1 copper cathode spot prices against the front-month 2503 contract were quoted at a discount of 110 yuan/mt to a discount of 50 yuan/mt, with an average price at a discount of 80 yuan/mt, up 20 yuan/mt MoM. According to SMM, only a slight inventory buildup occurred in the Shanghai region over the weekend, suggesting the current inventory buildup cycle may have ended. Currently, inventories in east China are near 300,000 mt, with downstream consumption showing a continuous recovery trend. Spot premiums are expected to rise further today.

(2) Guangdong: On March 3, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 60 yuan/mt to a premium of 20 yuan/mt, with an average price at a discount of 20 yuan/mt, up 10 yuan/mt MoM. Overall, suppliers were not eager to sell at the beginning of the month and stood firm on quotes, but actual transactions were moderate.

(3) Imported Copper: On March 3, warehouse warrant prices were $30-40/mt, QP March, with the average price flat MoM; B/L prices were $51-73/mt, QP April, with the average price up $5/mt MoM. EQ copper (CIF B/L) was quoted at -$4/mt to $4/mt, QP April, with the average price flat MoM. Quotes referenced cargoes arriving in mid-to-late March. Although the SHFE/LME price ratio improved yesterday, premiums for warehouse warrants and EQ copper remained suppressed at low levels. For B/L, premiums for two South American brands surged significantly due to large-scale purchases by some traders, with substantial transactions still occurring. The price spread between warehouse warrants and B/L widened.

(4) Secondary Copper: On March 3, secondary copper raw material prices rose by 200 yuan MoM. Guangdong bare bright copper prices were 70,700-70,900 yuan/mt, up 200 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,641 yuan/mt, up 77 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,025 yuan/mt. According to the SMM survey, copper prices fluctuated throughout the day. Although the price difference between primary and secondary copper rods widened slightly, downstream cargo pick-up remained slow. Some secondary copper rod enterprises saw a gradual increase in finished product inventories, with some even considering temporarily halting production.

(5) Inventory: On March 3, LME copper cathode inventories decreased by 1,025 mt to 261,050 mt. On the same day, SHFE warrant inventories decreased by 626 mt to 156,931 mt.

Prices: On the macro side, Trump announced that reciprocal tariffs would take effect on April 2, while the 25% tariffs on Mexico and Canada would be implemented on March 4, leaving no room for negotiation on tariffs with these two countries. Amid market concerns, the US dollar index declined throughout the day, providing support for copper prices. Additionally, with the resumption of work and production after the Chinese New Year, the February Caixin China Manufacturing PMI recorded 50.8, a three-month high. Positive domestic manufacturing data also boosted market confidence, pushing copper prices higher. On the fundamentals side, social inventories of copper cathode saw only a slight increase over the weekend, suggesting the current inventory buildup cycle may have ended. Downstream consumption showed some recovery but still has room for improvement. As of Monday, March 3, SMM's copper inventories in major regions nationwide increased slightly by 900 mt WoW to 377,000 mt, with total inventories up by 211,200 mt compared to the pre-holiday level of 165,800 mt. In summary, the US dollar index fell below the 107 mark, closing down 0.94%. Copper prices are expected to remain supported today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】